The Research and Development (R&D) Tax Incentive provides an opportunity for eligible companies to access claims for costs associated with R&D activities.

What is the R&D Tax Incentive?

R&D relief is provided in Australia through a tax based incentive program whereby the Australian Government provides companies with a tax offset (as opposed to a tax deduction) if they conduct eligible R&D activities (and spend at least $20,000 on such R&D activities). This offset is available annually on an ongoing basis to companies of all sizes and within all industry sectors. However, the size and nature of the offset differs depending on the turnover of the company as well as, from 1 July 2014, on the amount of R&D expenditure incurred.

Clients conducting R&D activities through non-corporate structures may therefore want to consider incorporating their business structures if they are conducting R&D activities, since the incentive is NOT available to businesses conducting R&D activities through trusts, partnerships or as individuals.

The incentive is generally only available for R&D activities conducted in Australia, but in certain circumstances it can also be available for R&D activities conducted outside Australia (broadly if the overseas activities have a significant scientific link to core R&D activities conducted in Australia and are not able to be conducted in Australia).

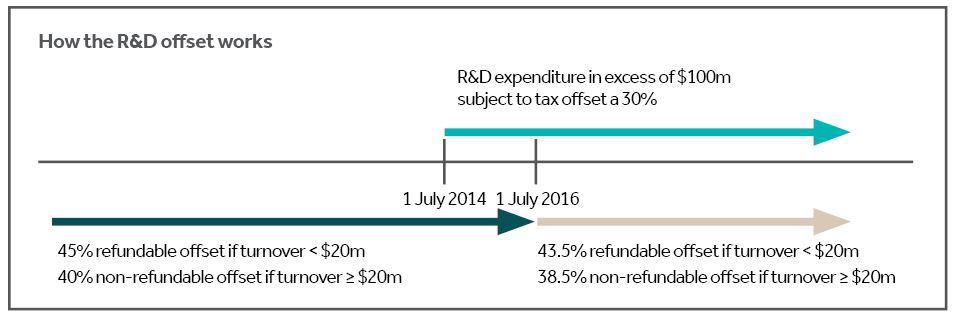

How does the R&D offset work?

A company can claim a tax offset for notional deductions such as expenditure incurred on eligible R&D activities and for the decline in value (and balancing adjustments) of depreciating assets used in R&D activities (provided the $20,000 spend requirement is met).

The size and the nature of the offset depend upon the company’s turnover and the amount of R&D expenditure incurred by the company:

For R&D expenditure up to $100 million:

- A company with a global turnover of less than $20 million can qualify for a 43.5% refundable offset (i.e. such smaller companies can receive a cash refund equal to 43.5% of the amount spent on eligible R&D activities, regardless of whether they are in a loss position or not); and

- A company with a global turnover of $20 million or more can qualify for a 38.5% non-refundable offset against tax payable (i.e. such companies which are in a loss position can carry forward their 38.5% offset to be deducted against tax payable in later years when they have a taxable income).

For R&D expenditure in excess of $100 million regardless of turnover, the tax offset will be limited to the company tax rate (i.e. 30%).

The 43.5% refundable offset available to smaller companies can therefore provide a cash injection to help start-ups that are often cash-strapped - for example, a startup company that is in a loss position for tax purposes who spends $1 million on R&D will receive a $435,000 cash refund under this incentive.

What are eligible R&D activities?

Broadly, eligible R&D activities will create new or improved materials, products, devices, processes or services and can consist of either:

- Only core R&D activities (broadly systematic experimental activities conducted to create new knowledge); or

- Both core and supporting R&D activities (broadly activities that relate to the core R&D activities).

Companies should meticulously document how they are conducting their R&D activities as well as keep records of their observations, evaluations and conclusions resulting from these activities.

Some examples of activities that are NOT core R&D activities (but may be supporting R&D activities) include:

- Reverse engineering or computer software for internal administration;

- Market research, management studies or research in humanities, social sciences or arts; or

- Mineral exploration or activities to comply with statutory requirements or standards.

What are the formalities to claim the R&D offset?

A company wanting to claim the R&D offset for an income tax year must lodge its registration with certain government departments (i.e. Innovation and Science Australia through AusIndustry) within 10 months of the end of the company’s income year (typically 30 April for 30 June year end).

To register, the company must provide details of all their R&D projects and core and supporting activities undertaken in the income tax year. It is therefore very important that the company keeps good records describing each activity, its planned objective, and the actual outcome as this will help a company to prove its eligibility in the event of a review or audit.

Once the company is registered, it can claim the R&D tax incentive when it lodges its tax return (that contains a R&D schedule). This schedule will contain details of all expenditure related to each R&D activity (e.g. even the wages of laboratory assistants, overheads relating to the R&D activity and consumables used in the process). It is therefore very important that the company keep good records (e.g. time sheets for staff costs) of all its R&D expenditure.

Industry experience

We have worked with clients from a range of industries to prepare, negotiate and agree on such applications from initial feasibility reviews to document submission, including:

- Mining and exploration

- Telecommunications

- Manufacturing

- Geospatial

- Aeronautical

- Software development

- Engineering

- Geological services

- IT/Technology

How Nexia can add value

Nexia Australia has the necessary skills and experience to assist you with all your R&D claims and record-keeping requirements to ensure you have the best chance of qualifying for the incentive.

We can assess the eligibility of a company’s business and projects (e.g. determine whether their activities are core or supporting R&D activities) and register the R&D activities with AusIndustry within 10 months of the end of the company’s income year (typically 30 April for 30 June year end) so that when the company lodges its company tax return and R&D schedule, it can claim its offset/refund from the ATO.

Working closely with your team, our dedicated R&D tax specialists can assist you with the following components:

- Identifying R&D tax core and supporting activities

- Evaluating R&D projects

- Calculating R&D Tax Incentive expenditure

- Calculating the tax offset of up to 45% of R&D spend

- Preparing R&D Tax Schedules for lodgement with your Income Tax Return

- Preparing R&D Plan documents (companies must maintain internal documents detailing their current R&D)

- Identifying appropriate process management and systems to ensure adequate R&D Tax documentation is retained

- Assistance in substantiating your R&D Tax claim

- Preparing advanced & overseas findings

- Evaluation of deferred franking debits Preparing 45% foreign rebate for Australian R&D costs

- Audit defence

- Dealing with compliance visits from either AusIndustry or the ATO.

- Application of the ‘feedstock’ provisions

- Determining if the ‘Not at Risk’ and ‘Clawback’ provisions apply to your circumstances

- Preparing a “position paper” or file note to support the claim

Substantiation and Process Improvement

Conducting R&D activities generates considerable documentation and the government requires a high level of substantiation of all activities claimed.

Our R&D team can provide expert advice regarding the documentation that must be maintained to support a robust R&D tax claim. In addition, our team can draw upon considerable expertise in order to improve your ability to identify, document and claim eligible R&D activities.

Intellectual property

All discussions are conducted with the highest sensitivity to the confidential nature of your intellectual property.

Your dedicated team

You will work with a professional team of taxation experts, and benefit from the high quality of service and technical knowledge expected of a larger firm, while enjoying the client focus and pricing of a mid-tier firm.

Pricing

Our costs can be determined on a fixed percentage of the claim (success fee) or a flat fixed fee.

Grant Application Assistance – Export Market Development

In addition to the R&D tax incentive program, there are other forms of financial assistance available to Australian businesses.

One such form of financial assistance is the Export Market Development Grant (EDMG) scheme - a Government program that provides Australian businesses with significant cash rebates for aspiring and current exporters. The scheme supports a wide range of industry sectors and products for the export of intellectual property and know-how outside Australia.

The following is a summary of the scheme:

- Encourages small and medium sized Australian business to develop export markets for their goods and/or services

- Reimbursement of up to 50% of the eligible expenditure incurred, above $5,000, provided that the total expenditure is at least $15,000, with up to eight grants available

- Maximum rebate of $150,000 per annum (subject to funds available in scheme)

- First time applicants can combine two years of expenses in their first claim

- Applications must be lodged by 30 November each year (no extensions available)

- Must have total annual turnover of less than $50 million

- Can include expenditure on international trade fairs, seminars, in-store promotions, international forums, promotional material and literature, advertising, overseas representatives, travel costs and communication.

We can identify eligible EMDG expenditure, prepare and lodge the application forms, and calculate the claim for maximum benefit.