Welcome to the newest edition of our Not-for-Profit Newsletter. Please feel free to contact us if you have any questions about the content of this Newsletter.

In this edition

This edition provides a reminder that public companies (including companies limited by guarantee) and large proprietary companies are required to have a whistleblower policy available to employees by 1 January 2020. ASIC has released guidance to assist in writing a policy to ensure the key mandatory components are covered. Whilst most charities will have lodged their June 2019 Annual Information Statements (AIS) by now, we remind charities that 31 January 2020 is the deadline and provide some tips on how to avoid common AIS mistakes.

As we have alerted in previous editions, the new Accounting Standards on Revenue Recognition and Leases are now in place and will apply to the financial statements of charities for the years ended 31 December 2019 and 30 June 2020. The Australian Accounting Standards Board staff have posted responses to frequently asked questions on the AASB website.

We also cover some items with respect to fraud and non-compliance with laws and regulations as well as the applicability of Single Touch Payroll for entities with less than 20 employees.

Click on one of the Newsletter sections below to Scroll to the Section

| Governance | ACNC activities | Financial reporting insights | Fraud and Non-compliance | Governments and the ATO |

ASIC guidance on whistleblower policies

The Australian Securities & Investments Commission has released guidance on writing a whistleblower policy for employees. Public companies, large proprietary companies and proprietary companies that are trustees of registrable superannuation entities were to have a policy available for officers and employees by 1 January.

Regulatory guide 270 Whistleblower policies help these companies establish policies that support and protect whistleblowers. The guide sets out legally binding components of a policy.

They include:

- Types of matters covered by a policy

- How to make a disclosure

- Who can make and receive a disclosure

- Legal and practical protections for disclosers

- Investigating a disclosure, and

- Ensuring fair treatment of individuals mentioned in a disclosure.

The guide also helps companies develop and implement policies that are tailored to their operations. ‘Robust and transparent whistleblower policies are essential to achieving sound risk management and corporate governance,’ said Commissioner John Price.

‘Whistleblower policies will influence behaviour and corporate culture in positive ways – for example, by encouraging greater disclosures of wrongdoing and by deterring people from doing the wrong thing. They play a crucial role in achieving a more fair and accountable corporate environment.’

ASIC does not require public companies that are not for profits or charities with annual revenue of less than $1 million to have a whistleblower policy. ‘We understand that these entities may face a compliance burden that outweighs the benefits a policy might otherwise offer,’ said Commissioner Price.

All companies are bound by whistleblower protections in the Corporations Act from 1 July 2019, regardless of whether they are required to have a whistleblower policy. ASIC plans to survey the policies of a sample of companies next year to review compliance.

Internal auditors pose NFP governance questions

The Institute of Internal Auditors – Australia has released a new guide for directors of NFPs, drafting 20 critical questions they should be asking. IIA-Australia CEO Peter Jones said the questions were a quick and easy reference for an estimated 257,000 Australian NFPs.

The Australian Charities and Not-for-profits Commission reported that charities’ annual revenue in the 2016 financial year was more than $142 billion, said Mr Jones. They remained among Australia’s most significant employers. ‘Good governance structures are as important in the charity and NFP sectors as it is in the financial-services sector,’ he added.

Mr Jones said that following investigations in 2017–18, the ACNC revoked the charity registrations of 22 organisations, the highest ever. Charities had corrected more than $20 billion in revenue and $354 million of assets to improve the accuracy of the charity register.

The 20 critical questions include:

- Is the NFP organisation’s governance framework contained in a formal document that adopts a holistic multidimensional approach to capture all structures and processes across the organisation: code of conduct and conflict-of-interest policy covering members, paid employees, non-paid volunteers and suppliers; strategic management, based upon risk and with strategically-based budget-setting; cash-reserves policy; risk management, insurance, fraud risks; resource management; information management; compliance and reporting; and audit and review?

- Have NFP organisational and fraud risks been identified? Are there appropriate risk-management actions in place, monitored and regularly reported to the board?

- Have governance activities, responsibilities and delegations been clearly defined, specifically for NFPs, and detailed in a fit-for-purpose governance document that is regularly reviewed and updated?

- How does the board gain assurance that all government and regulatory requirements have been identified and assigned, and that the NFP conforms with these requirements?

Another killer question: How does the NFP board know that its governance and assurance is operating effectively to ensure the organisation’s long-term sustainability?

All questions are available here.

What good local government integrity frameworks look like

A new 88-page research report shows how several local governments protect themselves against corruption. Released by the Independent Broad-based Anti-corruption Commission, Local government integrity frameworks review identifies a sample of councils that have built solid anti-corruption frameworks, providing models for other councils.

A key objective of IBAC’s review is to help councils strengthen their own measures against corruption.

IBAC found that six councils had sound frameworks and good practice in several areas. The commission reported that improvements could be made in others. Corruption risks were identified in procurement, cash handling, conflicts of interest, gifts, benefits and hospitality, employment practices, and misuse of assets and resources.

IBAC CEO Alistair Maclean said that the review was undertaken to show councils what a good integrity framework might look like. IBAC would support councils in examining their approaches and identify opportunities to improve their systems and controls to identify and manage corruption risks. ‘We recommend that all Victorian councils use the findings from this important review to assess their own integrity frameworks and identify where they can improve,’ Mr Maclean said.

‘Corrupt conduct by public-sector employees, including council employees, adversely affects the delivery of vital services and facilities. It wastes significant time and public money, meaning there is unfairness in the opportunity to provide services to councils, and damages reputations and community trust.’

The review showed that councils could improve on the development and communication of a clear policy on conflicts of interest, a broader consideration of corruption risks associated with employment practices, and ensuring that suppliers understood the probity standards expected of them.

The IBAC review also found that councils could do more to encourage reporting of suspected corrupt conduct. ‘It is critical that councils increase efforts to reassure employees they can be protected and that their report will be taken seriously,’ Mr Maclean said.

IBAC’s review sample included metropolitan, outer-metropolitan and regional councils. They were not identified. The review was not an audit, the focus being on good practice and potential opportunities for improvement.

The full report and summary are available here.

RSPCA NSW underpaid employees

The RSPCA in NSW says it underpaid 41 staff members by more than $120,000 due to a payroll error. The underpayment affected 22 of the animal-welfare charity’s 531 employees. Nineteen former employees were also underpaid.

An internal investigation began in 2017 when a staff member drew attention to potential errors.

A spokesman said: ‘It wasn’t a deliberate underpayment of staff or anything malicious. Certain employees were owed certain allowances based on their award that weren’t properly assessed or given at the time.’

The charity said it had gone to ‘significant effort to review every personnel file for each of our staff members to ensure that pay rates, classifications, allowances and other benefits are consistent with the relevant awards or agreements and the individual staff member’s letter of offer’.

Four external-conduct standards to comply with

Registered charities that operate overseas, including those classified as ‘basic religious’, must comply with four new external-conduct standards to maintain their ACNC registration.

Charities with activities outside Australia, however minor, must comply with them.

They operate in addition to existing governance standards.

The standards cover:

- How charities

- control their funds, goods and other resources

- The need for an annual review of overseas activities and record-keeping

- Anti-fraud and anti-corruption guidelines, and

- Measures aimed at protecting vulnerable individuals.

The ACNC has published guidance on the standards available here.

Unless requested, the commission does not require information specifically related to the new standards.

AIS deadline approaching fast

The 31 January deadline approaches for charities to file their 2019 annual information statements. This applies to charities running on a standard financial year (1 July to 30 June).

The 2019 Annual Information Statement Hub contains information a registered charity needs to provide to complete its AIS.

Support materials include:

- A guide to help complete each section of the statement, and

- A checklist that aims to help charities avoid common mistakes.

Charities are obliged to report annually, and filling out the statement is a key component of their obligations.

ACNC extends AIS due date for bushfire-affected

The ACNC has issued a blanket extension due date for the 2019 AISs for charities with an ‘address for service’ in designated fire-affected areas. They will now be due on 31 March 2020.

If you are in an area affected by bushfires, your postcode is not listed, and you require an extension of time to lodge, please contact Advice Services here and request an extension.

Avoiding common AIS mistakes

The ACNC has provided eight ways in which you can avoid errors in completing the 2019 AIS.

- Make sure your charity has completed last year’s statement before starting work on the next

- Check your charity’s fiscal year-end date to ensure that the correct reporting period is used

- Check your charity’s ‘address for service’ email – use a generic email address rather than a personal one

- Know what is needed if you’re a basic religious charity. The AIS contains several questions to help you determine if yours is a basic religious charity. Religious charities must advance religion and comply with five other requirements. Only a small number of charities that advance religion meet all five requirements. Read more here

- Ensure you select the right activities for your charity. A question allows charities to select ‘other categories’. Make this selection only in exceptional circumstances

- Remember to provide financial information

- Take up streamlined reporting opportunities. By answering questions about fundraising and incorporated-association details, many charities will no longer have to double-up and provide the same information to state and territory-based regulators. Have your charity’s incorporated association number as well as information about your organisation’s AGM, membership and fundraising handy so that you can answer these questions, and

- Look over your responses to AIS questions at the end of the form, and you may print out and review your AIS before submission to ensure you have completed it correctly. Remember to press the submit button. If you do not press submit, the commission will not receive the AIS. After you submit, you can save or print a PDF of your responses. The ACNC will also send you by email your responses.

Further tips follow for medium-sized charities that must submit a financial report that is either reviewed or audited. Large charities must submit a financial report that is audited.

- Know your financial-report type – general-purpose or special-purpose. Notes to financial statements must clearly state the type of financial report a charity has prepared. Ensure that accounting-policy disclosures highlight the type of financial report prepared

- Will you provide a consolidated financial statement? Although the ACNC accepts consolidated reports, don’t forget that the AIS’s financial information questions are only for the registered charities and not the entire group

- Attach all required documents

- If you prepare special-purpose financial statements, you must comply with the four mandatory accounting standards, and

- General-purpose statements must have complete and high-quality related-party disclosures. Ensure that all relevant accounting standards are complied with, and provide sufficient detail of transactions among related parties and key management personnel.

Year-enders must apply new standards

This year is big for NFPs that report in compliance with accounting standards.

The following complex accounting standards apply for annual reporting commencing on or after 1 January. Year-enders on 31 December are first cabs off the rank. The standards to watch out for are:

- AASB 15 Revenue from Contracts with Customers (NFP version)

- AASB 1058 Income of Not-for-profit Entities

- AASB 16 Leases, and

- AASB 2018-8 Amendments to Australian Accounting Standards – Right-of-Use Assets of Not-for-Profit Entities.

AASB 15 Revenue from Contracts with Customer is operative for NFPs for financial years that began on 1 January 2019. Implementation guidance and illustrative examples may be consulted.

The Australian Accounting Standards Board late last year issued amending standard AASB 2018-8 Amendments to Australian Accounting Standards – Right-of-Use Assets of Not-for-profit Entities, which affects leases.

AASB 2018-8 provides a temporary option for NFP lessees to elect to measure a class (or classes) of right-of-use assets arising under ‘concessionary leases’ at initial recognition, either:

- At cost, in accordance with AASB 16 Leases paragraphs 23–25, which incorporates the amount of the initial measurement of the lease liability, or

- At fair value (under AASB 13 Fair Value Measurement) in accordance with AASB 16 paragraph Aus25.1 (as amended).

There are important disclosure requirements where the ‘cost’ option is chosen. This extra information helps financial-statements users to assess:

- An entity’s dependence on leases that have significantly below-market terms and conditions principally to enable the entity to further its objectives, and

- The nature and terms of the leases, including lease payments, a description of underlying assets and restrictions on the use of underlying assets specific to the entity.

The information must be provided separately for each material lease that has significantly below-market terms and conditions principally to enable the entity to further its objectives or in aggregate for leases involving right-of-use assets of a similar nature.

You will need to consider the level of detail necessary to satisfy the disclosure objective and how much emphasis to place on each of the various requirements.

Remember to aggregate or disaggregate disclosures so that useful information is not obscured by either the inclusion of a large amount of insignificant detail or the aggregation of items that have substantially different characteristics.

If you are looking for the application of accounting standards, they are identified in AASB 1057 Application of Australian Accounting Standards. Its objective is to specify the types of entities and financial statements to which Australian Accounting Standards (including Interpretations) apply.

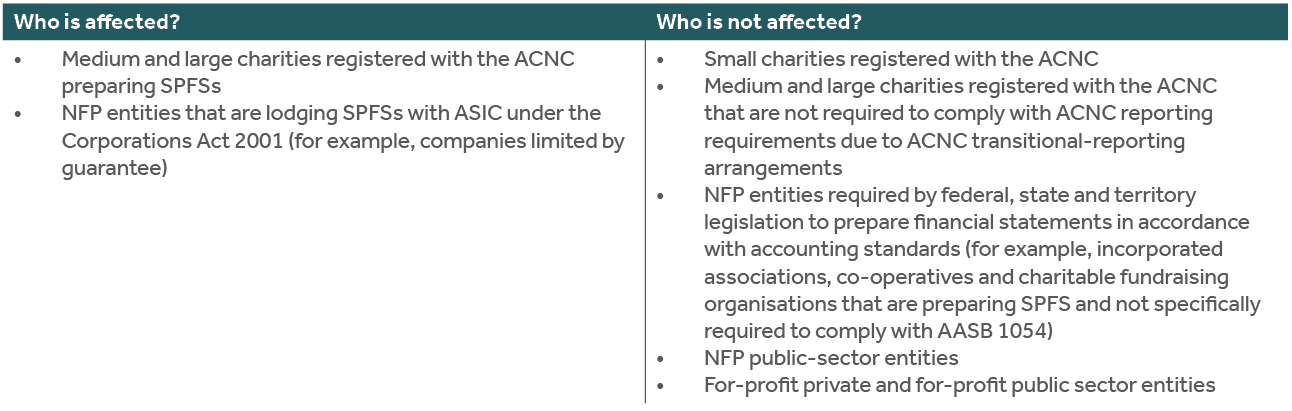

New disclosure requirements for some NFPs preparing SPFS

Under AASB 2019-4 Amendments to Australian Accounting Standards – Disclosure in Special Purpose Financial Statements of Not-for-Profit Private Sector Entities on Compliance with Recognition and Measurement Requirements new disclosures are required for annual reporting periods ending on or after 30 June.

The extra disclosures will provide clarity on compliance with the recognition and measurement requirements in Australian Accounting Standards.

Research has shown that the quality of disclosures in a significant number of special-purpose statements has not been sufficient to enable a user to determine what additional information they might need. For example, 44 per cent of medium and large charities lodging SPFSs with the ACNC failed to clarify whether or not they complied with recognition and measurement demands of accounting standards.

NFPs are not required to change existing accounting policies.

AASB 15 examples clarified

The AASB has decided to amend illustrative examples 4A and 4B attached to AASB 15 Revenue from Contracts with Customers to clarify how paragraph 35(a) should be applied.

The amendments do not change the examples’ conclusions.

A fatal-flaw-review version of the amending standard is expected to be issued shortly with a comment period of 30 days.

The board has also discussed a revised version of a draft staff FAQ presenting additional research-grant examples. Staff will meet with university and medical-research-sector stakeholders before finalising the FAQ.

Year-enders must apply new standards

AASB 15 Revenue from Contacts with Customer is operative for NFPs for financial years that began on 1 January. Implementation guidance and illustrative examples may be consulted.

Several other standards became operative from the same date, including AASB 1058 Income of Not-for-Profit Entities, AASB 16 Leases and AASB 2018-8 Amendments to Australian Accounting Standards – Right-of-Use Assets of Not-for-Profit Entities.

If you are looking for an application of accounting standards, they are identified in AASB 1057 Application of Australian Accounting Standards. Its objective is to specify the types of entities and financial statements to which Australian Accounting Standards (including Interpretations) apply.

You must disclose why you chose to prepare an SPFS.

Except for consolidation and equity accounting, for each material accounting policy applied and disclosed that does not comply with recognition and measurement requirements in Australian accounting standards, you must indicate where it does not comply, or disclose that an assessment of compliance has not been made, and whether or not the SPFS complies overall with the recognition and measurement requirements or state that such an assessment has not been made.

If the NFP entity has determined that its interests in other entities give rise to interests in subsidiaries, associates or joint ventures it must disclose whether or not it has consolidated or equity-accounted for those interests in accordance with the requirements in AASB 10 Consolidated Financial Statements and AASB 128 Investments in Associates and Joint Ventures. If it has not, it must say so and say why.

If the NFP entity has not made this assessment and was not required by legislation to do so, it must instead disclose that no assessment has been made.

Implementation guidance and illustrative examples to help preparers understand the new disclosures is available.

AASB staff post FAQs for NFPs

Australian Accounting Standards Board staff have posted eight new frequently-asked questions that will help NFPs.

They concern AASB 15 Revenue from Contracts with Customers, AASB 1058 Income of Not-for-Profit Entities and AASB 16 Leases.

They cover the standards’ scopes and effective dates, performance obligations under research grants, and identifying and recognising performance obligations in NFP schools.

Study spotlights NFP crime threat

Thousands of crimes targeting Australia’s NFPs are going unreported, a detailed study into not-for-profit governance has revealed. The Institute of Community Directors Australia’s latest Spotlight Report examines the impact of fraud and cybercrime on NFPs.

Informed by a nationwide survey of nearly 1900 community leaders, ICDA Spotlight Report: Fraud & Cybercrime shows that one in five organisations suffered a crime of some sort in the year leading up to the survey.

Applying those figures to an estimated 600,000 Australian NFPs – many of them small organisations with limited resources would suggest that as many as 114,000 organisations have been affected by fraud or cybercrime. Yet nearly two-thirds of those crimes are not reported to police, according to survey results, and just one in five is reported to an insurance company.

According to the study, asset theft and cyber-hacking are the most common crimes, followed by credit-card fraud and cash thefts. In about a quarter of asset theft cases, the perpetrator was either a staffer or a volunteer. Cash thefts were the most likely to be reported to the police.

Other serious crimes, such as payroll fraud, bribes, data theft or ransom, or expenses fraud were reported by less than 3 per cent of organisations. Online criminals perpetrated most credit-card fraud (59 per cent) and cyber attacks (53 per cent).

In a concerning result, the study found that up to 20 per cent of crime-affected organisations reported suffering several criminal incidents in a year. The largest proportion of uncovered fraud comes from staff whistleblowers.

Charities receiving bogus ACNC emails

Phishing emails that purport to be from the ACNC are being sent to some charities. They ask the charity to provide personal information. While the ACNC may request personal information from a charity, for example, in a registration application, charities should be wary about to whom they provide personal information.

If you receive an email purporting to be from the ACNC and are unsure of its legitimacy, call your registration analyst or the advice team on 13 22 62. Any request for information from the ACNC will include a signature block containing telephone and email contact details of the person sending the request.

Inquiry into ‘wages theft’

The Senate has referred terms of reference to its economics-references committee into the causes, extent and effects of unlawful non-payment or underpayment of employees’ remuneration.

The terms include:

- The forms of and reasons for wage theft and whether it is regarded by some businesses as ‘a cost of doing business’

- The cost of wage and superannuation theft to the national economy

- The best means of identifying and uncovering wage and superannuation theft, including ensuring that those exposing wage/superannuation thefts are adequately protected from adverse treatment

- The taxation treatment of people whose stolen wages are later repaid to them

- Whether the extension of liability and supply-chain measures should be introduced to drive improved compliance with wage and superannuation-related laws

- The most effective means of recovering unpaid entitlements and deterring wage and superannuation theft, including changes to laws that would assist with recovery and deterrence

- Whether federal government procurement practices can be modified to ensure that public contracts are awarded only to businesses that do not engage in wage and superannuation theft, and

- Any related matters.

The committee is to report to the senate by the last sitting day of June.

NFPs move to STP

If your NFP has 19 or fewer employees you will need to start reporting through Single Touch Payroll from 1 July. This means that you report your employees’ tax and superannuation information to the ATO each time you pay them.

The tax office has made several resources available to make the change, including a guide for small employers, a list of STP software providers and a news, events and resources page.

If your NFP has between one and four employees and doesn’t use payroll software, other ways to report STP information are:

- Implementing a no-cost and low-cost solution for STP that may include simple payroll software, mobile phone apps and portals, and

- Working with a registered tax or BAS agent. You may report your STP information quarterly simultaneously with business activity statements rather than each payday. Your tax or BAS agent will still need to report your STP information through an STP-ready solution. The option is available only until 30 June 2021.

For more information click here.

DGR reforms postponed

On 5 December 2017, the federal government announced reforms of the administration and surveillance of organisations with deductible-gift recipient status.

Changes were designed to strengthen governance arrangements, reduce administrative complexity and ensure continued trust and confidence in the NFP sector.

Initially planned for introduction on 1 July last year, reforms have been postponed until the same date this year. They will require non-government organisations with DGR endorsement to be registered charities (unless specifically exempted).

The reforms will also result in the transfer of four DGR registers to the ACNC. They are the:

- Register of environment organisations

- Register of cultural organisations

- The overseas aid-gift-deduction scheme, and

- Register of harm-prevention charities.