Introduction

Broadly, the superannuation guarantee (SG) legislation requires employers to make superannuation contributions equal to 9.5% of each employee’s ordinary time earnings at least quarterly. In the case of high-income earners, this minimum level of contributions can result in breaching the concessional contributions cap of $25,000, which has the effect of increasing the employee’s personal tax liability.

This is generally not a problem where there is only one employer involved, as the employer’s obligation to make SG contributions is capped by the maximum super contribution base, which is $55,270 per quarter in the 2020 financial year. However, some high-income earners, such as surgeons and other specialists who work at a number of hospitals during a year, receive super contributions from multiple employers which in total exceed their concessional contributions cap.

Recent legislation allows employees with more than one employer to apply to the ATO to opt-out of receiving SG contributions from some of their employers.

How it works

The employee can apply for one or more employers to be exempted from making SG contributions for one or more quarters by lodging an “SG opt-out for high-income earners with multiple employers” form with the ATO. The form must be lodged with the ATO at least 60 days before the beginning of the first quarter in which it is to apply, and can apply to up to four quarters in a financial year. A separate application is required for each financial year. There must be at least one employer who will continue to make SG contributions.

The deadline to apply for the quarter commencing 1 July 2020 is 10 May 2020.

The ATO will consider the application, and if satisfied, will issue an exemption certificate and issue written notice to the employee and each employer covered by the certificate. The ATO will only issue an exemption certificate if the employee is likely to exceed their concessional contributions cap, the employee will still have at least one employer obliged to make SG contributions in each quarter, and the combination of certificates sought is the most appropriate for the employee’s circumstances.

The employee can object against a decision by the ATO not to issue an exemption certificate, but this right is of questionable value given the length of time involved in resolving objections.

Some things to keep in mind

The issue of an exemption certificate removes the requirement under the SG legislation for an employer to make super contributions in the relevant quarter, but it is possible that an obligation to make contributions still exists under an award or workplace agreement, which is not affected by the exemption certificate.

An exemption certificate does not prevent the employer from continuing to make contributions if they choose to do so. Therefore, an employee can ask an employer to disregard an exemption certificate and recommence contributions if their circumstances change during the year. However, an exemption certificate cannot be varied or revoked once it is issued, so there is no mechanism to force an employer back into the SG system during the period of exemption.

The legislation does not specify how an employee should be compensated for the reduction in super contributions. It is therefore important that the employee discuss these issues with their employer, to ensure there is no misunderstanding.

Example

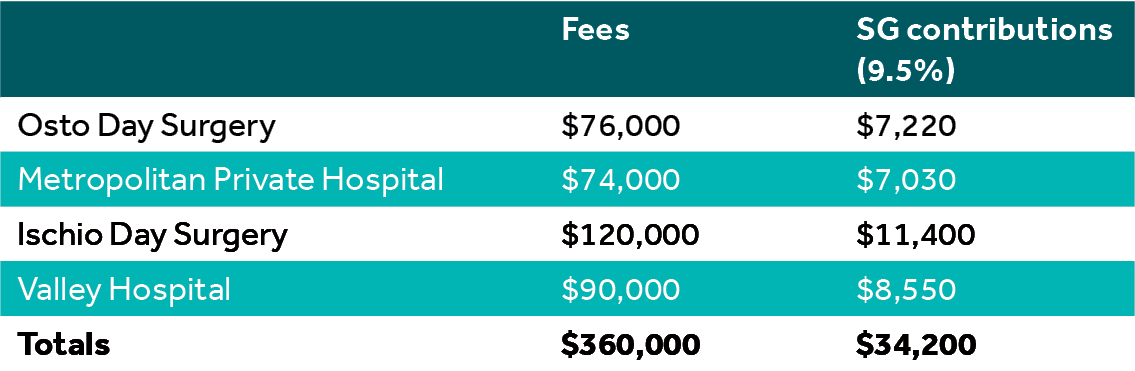

Robert is an orthopaedic surgeon who operates at different hospitals and is entitled to SG contributions equal to 9.5% of the fees he receives from each hospital. He expects in the 2021 financial year to receive the following fees and related SG contribution entitlements:

If all employers make the required SG contributions, Robert expects to exceed his concessional contributions cap by $34,200 - $25,000 = $9,200. If Robert takes no action, this excess will be included in his assessable income and taxed at his marginal rate.

If Robert wished to apply for an exemption for only one employer, the Ischio Day Surgery is the only single employer whose contributions are large enough to reduce the level of total contributions to below Robert’s concessional contributions cap. Alternatively, he might decide to apply for exemption for two of the smaller employers, however, the Explanatory Memorandum relating to the legislation states that “it might be appropriate for the Commissioner to deny an application for a certificate that would reduce [the employee’s] contributions by a substantially larger amount than is necessary, relative to another possible certificate”. It is not clear how the ATO will assess what is “a substantially larger amount”.

If you have any questions or wish to take advantage of this new concession, please contact your Nexia advisor.