The Chancellor of the Exchequer, Jeremy Hunt, has made some significant changes to the UK tax landscape. These updates coincidentally come ahead of the next UK general election, which will be called by 28 January 2025.

Highlights within this article include the following:

- Non-UK domiciled status is being abolished and replaced with a new four-year residency regime

- UK Capital Gains Tax (CGT) rate on property transactions reduced to 24%

- Furnished holiday letting abolished

- Stamp duty Multiple Dwellings Relief (MDR) abolished

- Further reductions in National Insurance Contribution (NIC) for employees and self-employed

- High-Income Child Benefit Charge (HICBC) threshold increased to GBP£80,000

- UK Individual Savings Account (ISA) for investment in UK Equities.

- Value Added Tax (VAT) threshold increased to GBP£90,000

Here, we have set out a summary of the key measures announced that may affect you and your business.

1. Non-domiciled individuals

New four-year residence based regime

The current UK remittance basis of taxation of non-UK domiciled individuals will be replaced with a new regime that will be based on the tax residence status of the individual.

Currently, non-UK domiciled individuals have the option to pay UK tax either on the arising basis (meaning taxed on their worldwide income and gains) or on their UK-sourced income and gains plus any foreign income and gains (FIG) that are brought into the UK. Currently, taxpayers can choose each year to be taxed either on the arising basis or remittance basis. The last year for which an individual can claim the remittance basis will be for the year 5 April 2025.

From 6 April 2025, qualifying individuals will be exempt from paying UK tax on their FIG, including the income and gains that are brought into the UK, during the first four-years of UK tax residence. Eligibility into this regime will apply to individuals who arrive in the UK only after a period of at least 10 years of non-UK tax residence. Eligibility into the regime is determined by UK tax residency only as opposed to their domicile position.

Individuals who have been UK tax resident in the UK for less than four-years on 6 April 2025 will be able to use this regime for any UK tax resident years in the remaining four-years. Reference will be determined under the UK’s Statutory Residence Test. Non-residence under a Double Tax Treaty with another country or years of split year tax residence, will be ignored for these purposes.

The new regime does not incur an annual charge (unlike the Remittance Basis Charge), but those individuals who claim to be taxed under this regime will still lose their UK tax-free income personal allowance and the UK CGT annual exemption.

Under a new Temporary Repatriation Facility (TRF), non-UK domiciled individuals who have been taxed on the remittance basis will be able to elect to pay UK tax on their foreign income at a reduced rate of 12% on remittances of pre-6 April 2025. TRF will be available for tax years to 5 April 2026 and 2027. TRF will not be available to FIG pre-6 April 2025, which are created within trusts and trust structures.

A one-year reduction will be available, from 6 April 2025, in the amount of FIG that is subject to UK tax for those individuals who switch from the remittance basis to the arising basis, and who are not eligible for the new four-year residence regime. As a result, only 50% of the foreign income arising during the year to 5 April 2026 will be subject to UK tax. The reduction will not apply to foreign chargeable gains.

Overseas Workday Relief (OWR)

OWR will be retained but simplified for the first three years of UK tax residence. OWR will be based on the employee’s tax residence position and whether they have opted to use the new four-year residence regime.

Capital Gains Tax (CGT) rebasing

From 6 April 2025, an individual who is not, or who later ceases to be, eligible for the new four-year FIG regime will be taxed on foreign gains in the normal way. Transitionally, individuals who have claimed the remittance basis and are neither UK domiciled or UK deemed domiciled by 5 April 2025 will, on a disposal of an asset held personally on 5 April 2019, be able to elect to rebase that asset to its value as at that date. This rebasing will be subject to conditions which are to be announced later.

Trust protections

Protection from UK tax on income and gains arising within settlor-interested trust structures will no longer be available for non-UK domiciled and deemed domiciled individuals who do not qualify for the four-year regime.

Inheritance Tax (IHT)

The UK government plans to move IHT from a domicile-based regime to a residence-based system, which would be effective from 6 April 2025. However, this is subject to consultation.

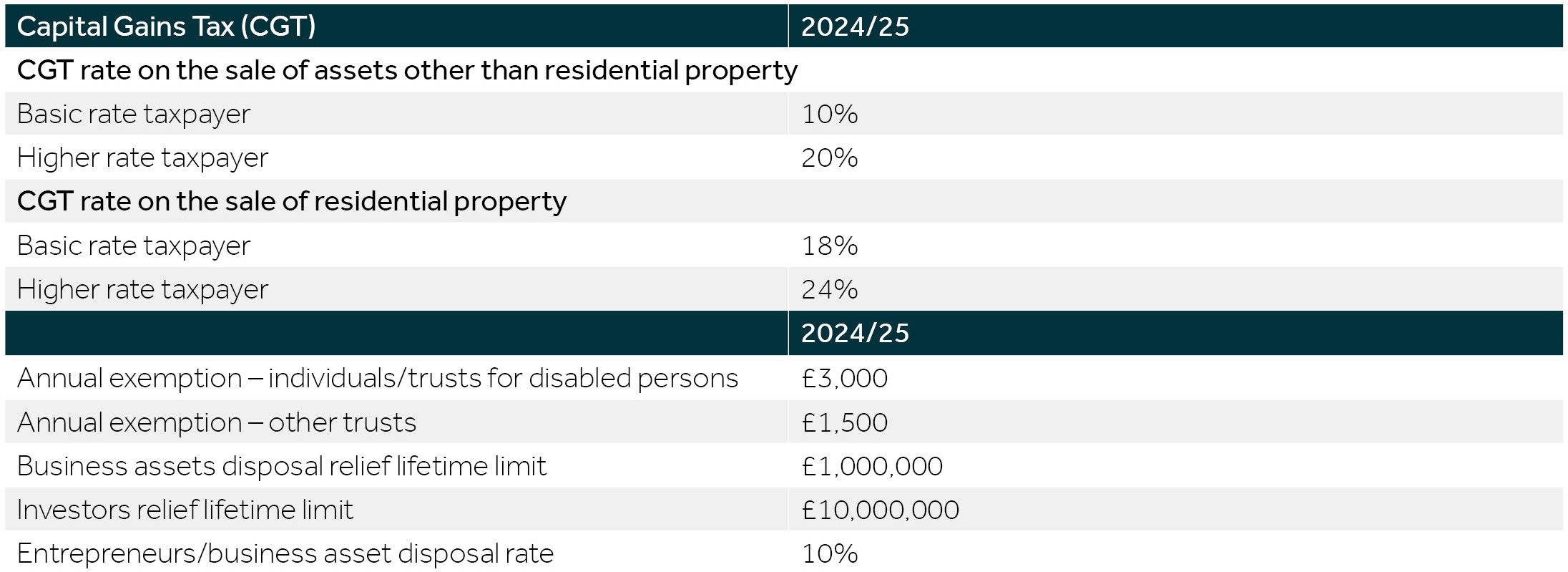

2. Reduction of CGT on sale of residential property

Currently the higher rate of UK CGT on the sale of UK residential property is 28%, but from the year to 5 April 2025 the rate will be reduced to 24%.

3. Abolishing furnished holiday let

Short-term and long-term let properties will be taxed the same from 6 April 2025. This means that individuals who own both Furnished Holiday Lets and non-Furnished Holiday Lets will no longer need to separately calculate and report their income. In addition, loan interest relief will not be able as a deduction for furnished holiday lets in the future, rather only a tax reducer will be available equivalent to basic rate (20%) tax relief.

4. Abolishing stamp duty relief

From 1 June 2024, Multiple Dwellings Relief (MDR) will be abolished. MDR is available for bulk land and property purchases under the UK Stamp Duty Land Tax regime.

For contracts exchanged on or before 6 March 2024, MDR will continue to apply, even if the purchase is completed on or after 1 June 2024.

5. National Insurance Contribution (NIC) reduction

The UK government has announced further reductions in NIC.

The main rate of Class 1 NIC for employees will be reduced from 10% to 8%. In addition, the Class 4 NIC for self-employed individuals will be reduced from 9% to 6%.

6. High Income Child Benefit Charge (HICBC) threshold increased

The HICBC is a UK tax charge applicable to UK households that claim child benefits where the income of the higher earner exceeds a certain threshold.

From 6 April 2024, the HICBC threshold will be increased to GBP£60,000 from GBP£50,000. In addition, where an individual or their partner’s adjusted net income is more than the taper top range, the child benefit will effectively be clawed back. This taper top rate has been increased to GBP£80,000.

7. UK Individual Savings Account (ISA) for investment in UK Equities

UK resident individuals will be able to contribute up to GBP£5,000 tax-free into a new UK Individual Savings Account (ISA). This tax-free product is designed for individuals to invest purely in UK-focused assets. This new UK ISA will be in addition to the existing ISA allowance of GBP£20,000 limit.

8. Value Added Tax (VAT) threshold increase

To support small businesses and sole traders in the UK, the VAT registration threshold will be increased from GBP£85,000 to GBP£90,000. In addition, the VAT deregistration threshold will be increased to GBP£88,000 from GBP£83,000 from 1 April 2024.

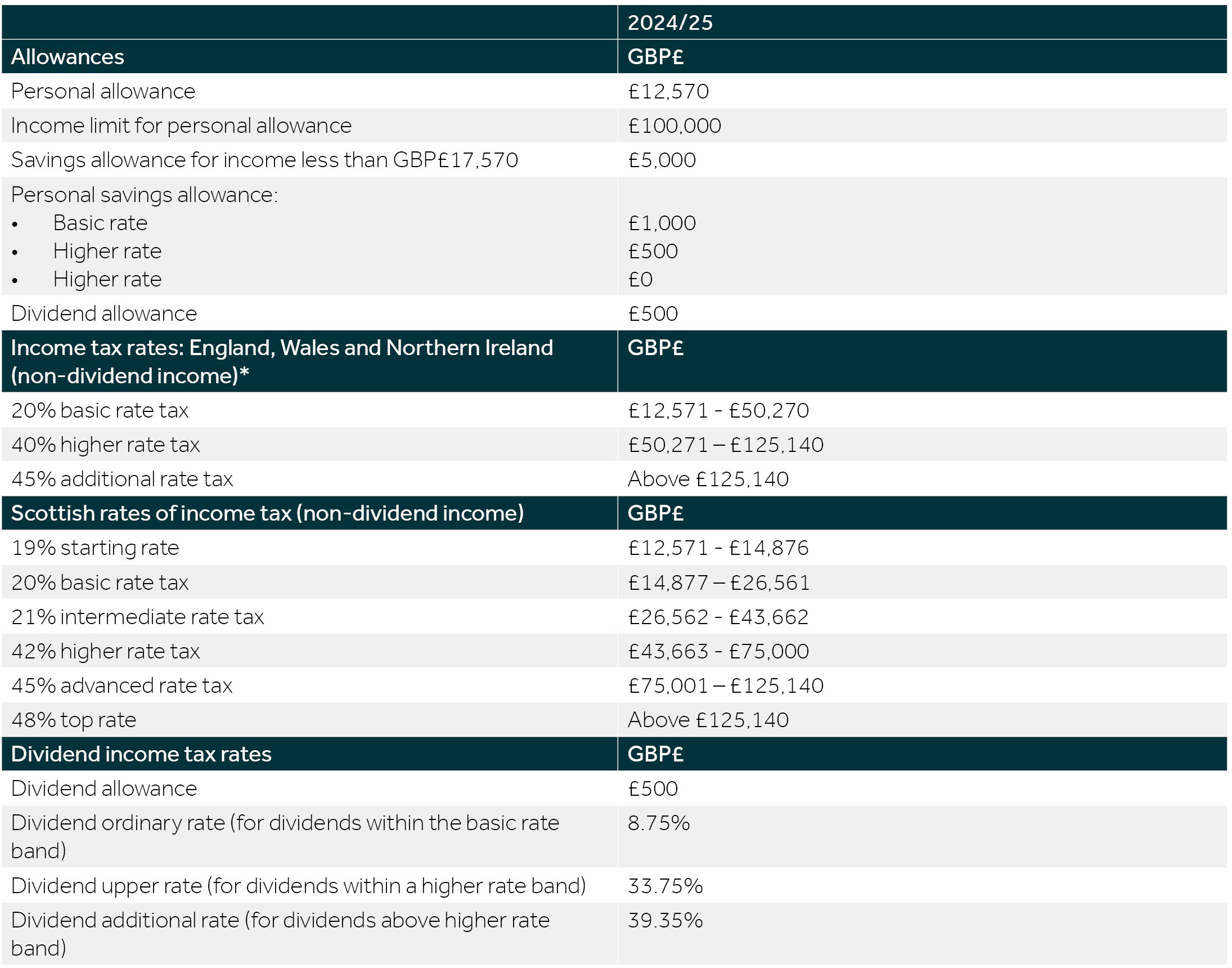

Income tax rates

The personal tax thresholds remain frozen until April 2028.

We've included a summary of the UK tax rates along with the main allowances outlined in the table below.

*Note the UK Personal allowance abates by £1 for every £2 of income above £100,000 p.a.

Capital Gains Tax (CGT)

We've included a summary of the CGT rates and main reliefs in the below table.

Next steps

Speak with your local Nexia Advisor today to learn more or if you have any questions regarding the items listed in this article. At Nexia, we're here to help you connect with your true potential and navigate towards your goals.